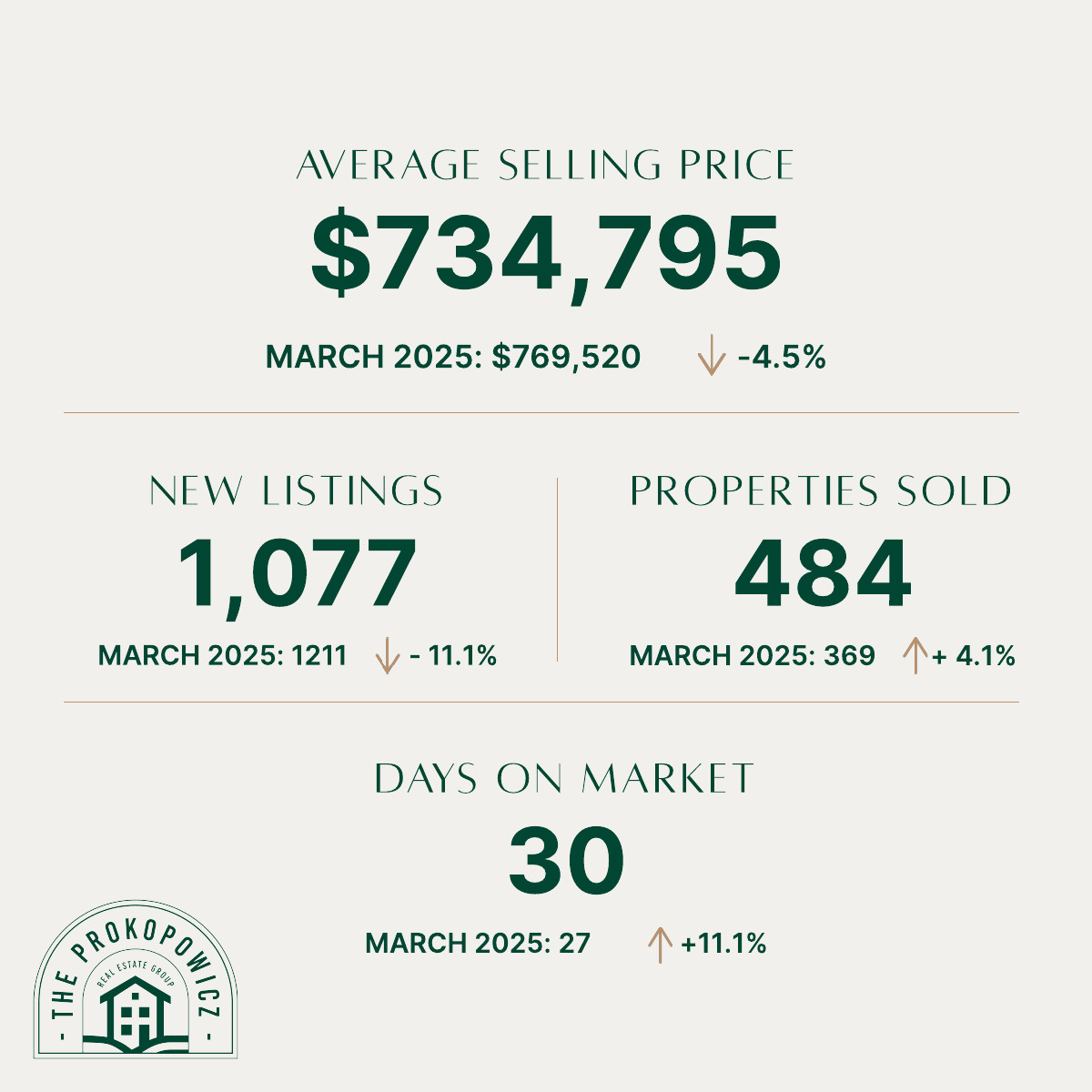

The spring market has arrived in Waterloo Region. As expected with the seasonal shift, March brought the typical pickup in both sales and new listings — up 39.4% and 44.8% month-over-month respectively, reflecting the natural rhythm of buyers and sellers re-engaging after the quieter winter months. The more telling signal is year-over-year: sales are up 4.1% compared to March 2025, a meaningful indicator that underlying demand in the region is strengthening, not just seasonally active.

“Waterloo Region’s market is gaining momentum with significant sales growth and robust new listing activity. The Kitchener-Waterloo benchmark price experienced a modest month-over-month HPI gain, while the Cambridge benchmark price saw a slight decline. Combined with more constrained inventory levels than in many other areas, working with a local REALTOR® who understands Waterloo Region’s market nuances is paramount.”

— Bill Duce, CEO, Cornerstone

Price trends: stability with nuance

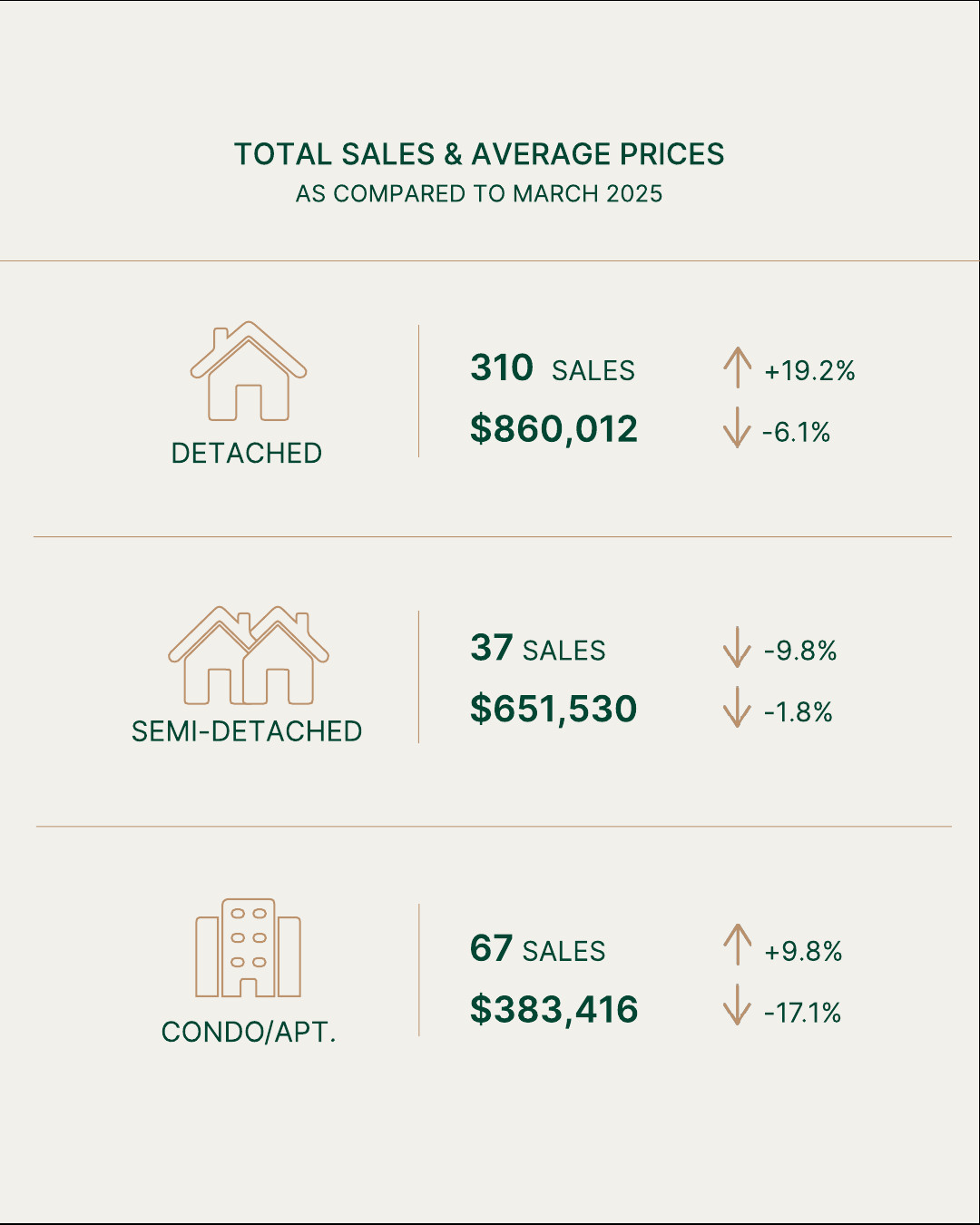

The headline price story in March is one of stability, with slight variation depending on where you look. The average sale price across the region came in at $733,258 — down 4.4% year-over-year, but consistent with the gradual price consolidation seen over the past several months.

Kitchener-Waterloo:

+0.5% month/month

−8.8% year/year

Cambridge:

−1.0% month/month

−7.7% year/year

The MLS® HPI (Home Price Index) — which strips out extreme sales to give a cleaner picture — shows Kitchener-Waterloo nudging upward by 0.5% in March, while Cambridge dipped 1.0%. Both sub-markets remain below last year’s levels, but the year-over-year gaps have been narrowing. This suggests prices are finding a floor rather than continuing to fall.

Supply: still tight, still significant

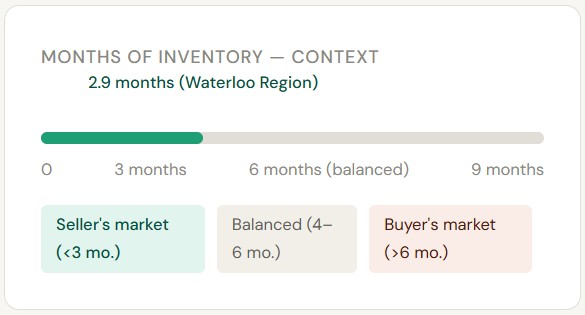

Months of supply — Waterloo Region (approx. context)

Waterloo Region (March 2026) Balanced market range (4–6 months)

Inventory across the region dropped 11.6% year-over-year, leaving 2.9 months of supply — essentially the same level as March 2025. But that 2.9-month figure is a regional average, and averages can obscure as much as they reveal. The market is not moving at one speed: detached homes and condos are operating in meaningfully different conditions, and what’s true for one property type may not be true for another.

Detached homes — particularly well-located, move-in ready properties — continue to see stronger demand relative to supply. Condos, on the other hand, are sitting longer as buyers in that segment have more options and more patience. If you’re buying or selling a condo, you’re navigating a different market than someone dealing in detached homes, and your strategy should reflect that.

What ties both segments together is this: pricing correctly is paramount. With homes averaging 30 days on market — up 11.1% year-over-year — today’s buyers are doing their homework. Overpriced listings are being passed over regardless of property type, while accurately priced homes are still moving with purpose. In a market with this much internal variation, the difference between a well-priced listing and an aspirationally priced one isn’t just time — it’s often thousands of dollars in eventual reductions and carrying costs.

What this means for buyers & sellers

For Buyers:

More choice, but move with intention

Spring has brought fresh inventory — new listings are up 44.8% from February, giving you the best selection since fall. Prices are 4–8% below last year’s levels. That said, supply is still tight at 2.9 months, so well-priced homes aren’t sitting long. Come pre-approved, understand the local sub-markets, and be ready to act when the right property appears.

For Sellers:

Spring momentum is real — price sharp

The seasonal pickup is underway, and with sales up 4.1% year-over-year, this spring has real substance behind it. Inventory remains lean, giving well-prepared sellers an edge. The key: price accurately against today’s benchmarks, not 2022 peaks. Homes priced to current market conditions are selling within 30 days. Overpriced listings are lingering while comparable homes pass them by.

The Waterloo Region continues to demonstrate resilience that many other Ontario markets can’t claim. A combination of growing employment, post-secondary anchor institutions (University of Waterloo, Wilfrid Laurier, Conestoga College), and tech-sector depth means demand here has a structural floor. March’s numbers reflect that foundation starting to reassert itself as we head into the traditionally active spring season.

Ready to make your move?

Every neighbourhood in Waterloo Region tells a slightly different story. As local Realtor’s we can help you read the data that matters for your specific situation — whether you’re buying your first home in Cambridge or listing a family home in Kitchener.

*Statistics as of April 6, 2026. Source: KWAR MLS® System.